Morning ORB FVG Trigger✅ Overview

Morning ORB FVG Trigger is a complete intraday trading framework built around:

A Morning Opening Range Breakout (ORB)

The first Fair Value Gap (FVG) after that breakout

Strict risk management and position sizing

Optional HTF trend filter (Daily / Weekly / Monthly)

Optional Daily ATR filter to avoid extreme days

The script is designed for futures / indices / FX on intraday charts up to 15 minutes and for traders who want a clean, mechanical entry framework with clear risk.

🧠 Core idea

Define a morning opening range (e.g. 09:30–09:45).

Wait for a clean breakout above/below that range.

After the breakout, wait for the first FVG in breakout direction,

confirmed by the next candle (no immediate full reclaim).

Use a chosen stop logic + R:R factor to build risk/reward boxes.

Calculate position size based on your account risk.

(Optional) Only take trades:

In the direction of the HTF EMA trend (D/W/M).

On days where the morning range is within a band of the Daily ATR.

You can also disable all signals/boxes and use the script just as a visual ORB tool.

⏰ 1. ORB / Morning Range

Inputs (Main section)

Morning Range Session

Time window of the opening range in exchange time

Example: 09:30–09:45 for a 15-minute ORB.

You can type custom ranges (e.g. 09:30–09:35 for a 5-minute ORB).

Risk/Reward (TP factor)

Multiplier for the take-profit distance relative to the stop.

2.0 = TP is 2× the stop distance

1.5 = TP is 1.5× the stop distance

Show ORB range

If enabled, draws:

ORB high/low lines

ORB labels (e.g. 15min ORB high / low)

Optional midline

Extend ORB lines to the right (bars)

How many bars to extend the ORB high/low horizontally beyond the ORB itself.

Trade box width (bars)

Horizontal width (in bars) of:

Red risk box (entry–stop)

Green reward box (entry–TP)

Implementation details

The ORB is always calculated on 1-minute data internally, so it stays precise even on 5m/15m charts.

The script only works on intraday timeframes up to 15 minutes.

📦 2. FVG Block

Group: “FVG”

Threshold %

Minimum size of an FVG in % of price.

0 = every FVG

Higher values = only larger gaps

Auto threshold (from volatility)

If enabled, the minimum FVG size is derived from historical volatility

instead of a fixed percentage.

Allow breakout FVG partly inside ORB

Off (default): the FVG must lie fully outside the ORB.

On: the breakout FVG itself may still overlap the ORB a bit,

as long as it is the first one attached to the breakout move.

Enable FVG entry signals, boxes & alerts

On: full system – FVG detection, entry labels, risk/TP boxes, alerts.

Off: no entries, no risk/TP boxes, no alerts.

You only get the ORB and (optionally) the HTF dashboard, so you can trade your own setups.

Entry mode

Entry mode (Mid / Edge / NextOpen)

Mid – Entry at the midpoint of the FVG.

Edge – Long at the upper FVG edge, short at the lower FVG edge.

NextOpen – No limit order in the gap. Entry is placed at the next bar open after FVG confirmation.

Edge offset (ticks)

Additional offset for Edge entries:

Long:

+ticks = a bit above the FVG (more conservative)

-ticks = deeper into the FVG (more aggressive)

Short:

+ticks = a bit below the FVG

-ticks = deeper into the FVG

FVG detection logic

Uses a LuxAlgo-style 3-candle FVG pattern (gap between candle 1 and 3).

Only one FVG is taken: the first valid FVG after the ORB breakout in breakup direction.

The FVG candle is the middle bar; the script:

Detects the FVG on the previous bar.

Waits for the current bar to confirm it:

Bullish: current low must stay above the lower FVG boundary

Bearish: current high must stay below the upper FVG boundary

Only then an entry signal is generated.

🛑 3. Stop Logic

Group: “Stop Logic”

Stop mode (PrevBar / Pivot / FVG Candle)

PrevBar – Stop at the low/high of the candle before the FVG

(tight/aggressive).

FVG Candle – Stop at the low/high of the FVG candle itself

(medium).

Pivot – Stop at the most recent swing high/low

using pivotLeft / pivotRight pivots (more conservative).

Ticks (stop buffer)

Offset (in ticks) from the selected stop level.

> 0 = further away (more room, more risk)

< 0 = closer (tighter stop)

Pivot left / Pivot right

Number of candles left/right to define a swing high/low

when using Pivot stop mode.

Typical intraday values: 2–3.

The script also sanity-checks the stop:

if the calculated stop would be invalid (e.g. above entry in a long), it moves it by a minimal distance (2 ticks) to keep a valid risk.

📈 4. HTF Trend Filter (Daily / Weekly / Monthly)

Group: “HTF Trend Filter”

Enable HTF trend filter

If enabled, trades are only allowed:

Long when at least 2 of D/W/M closes are above their EMA

Short when at least 2 of D/W/M closes are below their EMA

EMA length (D/W/M)

EMA length for all three higher timeframes (Daily, Weekly, Monthly).

This helps focus entries in the direction of the dominant higher-timeframe trend.

📊 5. ATR Filter (Daily)

Group: “ATR Filter (Daily)”

Use daily ATR filter

If enabled, the height of the ORB (ORB high – ORB low) must be within

a band of the Daily ATR to allow any signals.

Daily ATR length

ATR period on the Daily timeframe.

Min ORB size vs ATR

Lower bound:

Example: 0.3 → ORB must be at least 0.3 × Daily ATR

0.0 = no minimum.

Max ORB size vs ATR

Upper bound:

Example: 1.5 → ORB must be ≤ 1.5 × Daily ATR

0.0 = no maximum.

If the ORB is too small (choppy) or too large (exhausted move), no breakout or FVG signal will be generated on that day.

🧭 6. HTF Dashboard & Signal Labels

Group: “HTF Trend Dashboard”

Show HTF dashboard

Draws a small label at the top of the chart showing:

HTF Trend (EMA X)

D: UP/FLAT/DOWN

W: UP/FLAT/DOWN

M: UP/FLAT/DOWN

Dashboard position

Top Right, Top Center, Top Left – places the dashboard at the top.

Over Risk Info – no top dashboard; instead, the HTF trend info is shown as a label near the risk box when a new signal appears.

Lookback (bars) for top anchor

How many bars to use to determine the top price level for dashboard placement.

Show HTF trend above risk box on signal

Only relevant if Dashboard position = Over Risk Info.

When enabled, a small HTF label appears near the risk box for each new trade.

Signal label vertical offset (ticks)

Vertical spacing between risk info label and HTF label.

Minimum spacing HTF/Risk (ticks)

Ensures a minimum vertical distance so the two labels don’t overlap.

HTF signal label X offset (bars)

Horizontal offset (left/right) relative to the risk info label.

⏳ 7. ORB–FVG Filters (Session & Time Window)

Group: “ORB FVG Filter”

Only same session day

If enabled, FVG entries are only allowed on the same calendar day

as the ORB. When the date changes, all state & drawings are reset.

Limit hours after ORB

Enables a time window after the ORB end.

Trading window after ORB (hours)

Length of that window in hours.

Example: 2.0 → FVG signals only in the first 2 hours after ORB end.

💰 8. Risk Management & Position Sizing

Group: “Risk Management”

Calculate position size

If enabled, the script computes suggested mini and micro contract size for you.

Account size

Your trading account size (in account currency).

Risk mode

Percent – risk is a % of account size (Account risk %).

Fixed amount – risk is a fixed dollar amount (Fixed risk ($)).

Account risk %

Risk per trade as a percentage of account size (e.g. 1.0 for 1%).

Fixed risk ($)

Fixed risk per trade in dollars when using Fixed amount mode.

Micro factor (vs mini)

How much a micro contract is worth relative to a mini.

Example:

0.1 → one micro moves 1/10 of one mini.

Risk Info label

For each new trade, a label is shown above the boxes with:

Stop distance in price and $ risk per mini

Max risk allowed for the trade

Suggested mini and micro size

Text like:

Suggested: 2 mini

Suggested: 5 micro

or Suggested: no trade

This makes the script especially useful for prop-firm rules or strict risk discipline.

🎨 9. Visual Style (Boxes, Labels, ORB Lines)

Group: “Box & Label Style (Trade)”

Label font size (Very small, Small, Normal, Large)

Entry label BG / text color

Stop label BG / text color

TP label BG / text color

Risk info BG / text color

Risk box color (entry–stop zone)

Reward box color (entry–TP zone)

Group: “ORB Style”

ORB high line color

ORB low line color

ORB line width

ORB label font size

ORB label background color

ORB label text color

Show ORB midline

ORB midline color / width / style (Solid / Dashed / Dotted)

⚠️ 10. Alerts

Group: “Alerts”

The script defines three alert conditions:

Long entry FVG breakout

Triggered when a new long signal appears.

Short entry FVG breakout

Triggered when a new short signal appears.

FVG entry (long/short)

Generic alert for any new signal (long or short).

To use them:

Add the indicator to the chart.

Open the Alerts dialog → “Condition”.

Select this script and one of the alert conditions.

Set your preferred expiration and notification settings.

Alerts only fire when Enable FVG entry signals, boxes & alerts is on.

🧩 11. How the trading logic flows (summary)

Build ORB on 1-minute data during the selected session.

Optionally reject the day if ORB is outside the ATR bounds.

Wait for a breakout (close above high or below low), respecting HTF trend filter.

After breakout, look for the first valid FVG in that direction:

Outside the ORB (unless breakout FVG allowed inside)

Confirmed by the next candle (no full reclaim)

Once confirmed:

Compute entry, stop, target.

Draw risk/reward boxes and all labels.

Optionally show HTF signal label over the risk info.

Trigger alerts if enabled.

If you disable FVG signals, only steps 1–3 (plus dashboard) are effectively active.

⚠️ 12. Notes & Disclaimer

Script is intended for intraday trading up to 15-minute timeframes.

All signals are mechanical and do not guarantee profitability.

Always backtest and forward-test on your own data before risking real money.

This script is for educational purposes only and is not financial advice.

🚀 Quick-start guide

Add the script to your chart

Use an intraday timeframe ≤ 15 minutes (1m, 3m, 5m, 15m).

Works best on liquid indices, futures, FX and large-cap stocks.

Set the Morning Range

In “Morning Range Session” choose the exchange’s opening window.

Examples

US index futures (CME): 08:30–08:45 or 08:30–08:35

US stocks (NYSE/Nasdaq): 09:30–09:45 or 09:30–09:35

The ORB is always calculated on 1-minute data internally, so the range stays accurate on higher intraday charts.

Keep the default filters at first

HTF Trend Filter: ON

EMA length = 20

This will only allow trades in the direction of the dominant D/W/M trend.

ATR Filter: OFF (optional; you can enable later once you’re comfortable).

Use the full trade system

In the FVG group leave

“Enable FVG entry signals, boxes & alerts” = ON

Entry mode: Mid

Stop mode: FVG Candle or PrevBar

Risk/Reward: 2.0 as a starting point.

Set your risk

Turn on “Calculate position size”.

Enter your Account size and choose either:

Risk mode = Percent (e.g. 1.0 = 1% per trade), or

Risk mode = Fixed amount (e.g. $250 per trade).

The risk info label will show:

Stop distance in price and $/contract

Max allowed risk

Suggested mini and micro contract size.

Enable alerts (optional)

Open the Alerts dialog → Condition: this script.

Choose one of:

Long entry FVG breakout

Short entry FVG breakout

FVG entry (long/short)

Choose “Once per bar” or “Once per bar close”, and your preferred notification type.

Replay & journal

Use the TradingView bar replay tool to step through past days.

Focus on:

How the ORB defines the structure.

How the first confirmed FVG outside the ORB behaves.

Whether the risk/TP levels fit your own style and product.

🎛 Recommended settings & profiles

These are starting points, not rules. Always adapt to the instrument and your own risk tolerance.

1. Conservative / Trend-following

Timeframe: 5m or 15m

Morning Range Session: 15-minute ORB around the cash or futures open

FVG

Threshold %: 0.05–0.1 (filter out very small gaps)

Auto threshold: OFF (keep it simple)

Allow breakout FVG partly inside ORB: OFF

Enable FVG entry signals/boxes/alerts: ON

Entry mode: Mid

Stop Logic

Stop mode: Pivot

Pivot left/right: 2–3

Stop buffer: +1–2 ticks

HTF Trend Filter

Enabled: ON

EMA length: 20

ATR Filter

Enabled: ON

Daily ATR length: 14

Min ORB vs ATR: 0.3–0.4

Max ORB vs ATR: 1.2–1.5

Risk Management

Risk mode: Percent

Account risk: 0.5–1.0%

Idea: Only trade when the higher-timeframe trend supports the move and the opening range is of a “normal” size for the current volatility.

2. Balanced / Intraday directional

Timeframe: 3m or 5m

FVG

Threshold %: 0.02–0.05

Auto threshold: ON (lets the script adapt to volatility)

Allow breakout FVG partly inside ORB: ON

(first breakout FVG may partly sit inside the ORB)

Entry mode: Edge

Edge offset (ticks): 0 or +1

Stop Logic

Stop mode: FVG Candle

Stop buffer: 0–1 ticks

HTF Trend Filter

Enabled: ON

ATR Filter

Enabled: OFF (optional)

Risk Management

Risk mode: Percent

Account risk: 1.0–1.5% (if this fits your plan)

Idea: Slightly more aggressive entries at the gap edge, still aligned with HTF trend, but with more flexibility on ATR.

3. Aggressive / Scalping around the ORB

Timeframe: 1m or 3m

FVG

Threshold %: 0.0–0.02

Auto threshold: ON

Allow breakout FVG partly inside ORB: ON

Entry mode: NextOpen or Edge with a negative offset (deeper into the gap)

Stop Logic

Stop mode: PrevBar

Stop buffer: 0 or -1 tick

HTF Trend Filter

Enabled: OFF (or ON but treat as soft guidance)

ATR Filter

Enabled: OFF

Risk Management

Risk mode: Percent

Account risk: lower, e.g. 0.25–0.5% per trade

Idea: More trades and tighter stops. Best for experienced traders who understand the limitations of scalping and whipsaw risk.

Final reminder

All of these are templates, not guarantees:

Always check how the system behaves on your market and session.

Start on replay and demo before trading real money.

Adjust filters (HTF, ATR, thresholds) until the signals fit your personal approach.

Pesquisar nos scripts por "THE SCRIPT"

Material Color Palette Library█ OVERVIEW

Unlock a world of color in your Pine Script® projects with the Material Color Palette Library . This library provides a comprehensive and structured color system based on Google's Material Design palette, making it incredibly easy to create visually appealing and professional-looking indicators and strategies.

Forget about guessing hex codes. With this library, you have access to 19 distinct color families, each offering a wide range of shades. Every color can be fine-tuned with saturation, darkness, and opacity levels, giving you precise control over your script's appearance.

To make development even easier, the library includes a visual cheatsheet. Simply add the script to your chart to display a full table of all available colors and their corresponding parameters.

█ KEY FEATURES

Vast Spectrum: 19 distinct color families, from vibrant reds and blues to subtle greys and browns.

Fine-Tuned Control: Each color function accepts parameters for `saturationLevel` (1-13 or 1-9) and `darkLevel` (1-3) to select the perfect shade.

Opacity Parameter: Easily add transparency to any color for fills, backgrounds, or lines.

Quick Access Tones: A simple `tone()` function to grab base colors by name.

Visual Cheatsheet: An on-chart table displays the entire color palette, serving as a handy reference guide during development.

█ HOW TO USE

As a library, this script is meant to be imported into your own indicators or strategies.

1. Import the Library

Add the following line to the top of your script. Remember to replace `YourUsername` with your TradingView username.

import mastertop/ColorPalette/1 as colors

2. Call a Color Function

You can now use any of the exported functions to set colors for your plots, backgrounds, tables, and more.

The primary functions take three arguments: `functionName(saturationLevel, darkLevel, opacity)`

`saturationLevel`: An integer that controls the intensity of the color. Ranges from 1 (lightest) to 13 (most vibrant) for most colors, and 1-9 for `brown`, `grey`, and `blueGrey`.

`darkLevel`: An integer from 1 to 3 (1: light, 2: medium, 3: dark).

`opacity`: An integer from 0 (opaque) to 100 (invisible).

Example Usage:

Let's plot a moving average with a specific shade of teal.

// Import the library

import mastertop/ColorPalette/1 as colors

indicator("My Script with Custom Colors", overlay = true)

// Calculate a moving average

ma = ta.sma(close, 20)

// Plot the MA using a color from the library

// We'll use teal with saturation level 7, dark level 2, and 0% opacity

plot(ma, "MA", color = colors.teal(7, 2, 0), linewidth = 2)

3. Using the `tone()` Function

For quick access to a base color, you can use the `tone()` function.

// Set a red background with 85% transparency

bgcolor(colors.tone('red', 85))

█ VISUAL REFERENCE

To see all available colors at a glance, you can add this library script directly to your chart. It will display a comprehensive table showing every color variant. This makes it easy to pick the exact shade you need without guesswork.

This library is designed for fellow Pine Script® developers to streamline their workflow and enhance the visual quality of their scripts. Enjoy!

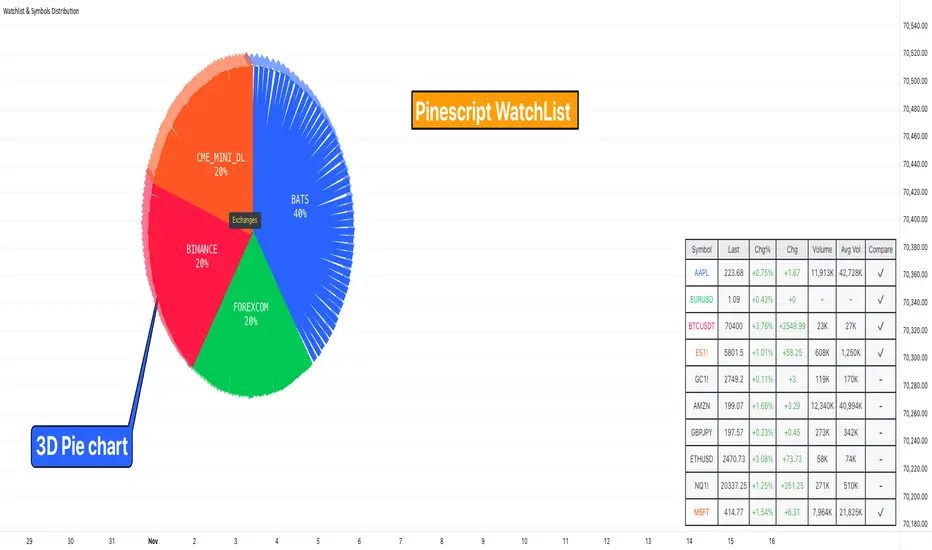

Watchlist & Symbols Distribution [Daveatt]TLDR;

I got bored so I just coded the TradingView watchlist interface in Pinescript :)

TLDR 2:

Sharing it open-source what took me 1 full day to code - haven't coded in Pinescript in a long time, so I'm a bit slow for now :)

█ OVERVIEW

This script offers a comprehensive market analysis tool inspired by TradingView's native watchlist interface features.

It combines an interactive watchlist with powerful distribution visualization capabilities and a performance comparison panel.

The script was developed with a focus on providing multiple visualization methods while working within PineScript's limitations.

█ DEVELOPMENT BACKGROUND

The pie chart implementation was greatly inspired by the ( "Crypto Map Dashboard" script / )

adapting its circular visualization technique to create dynamic distribution charts. However, due to PineScript's 500-line limitation per script, I had to optimize the code to allow users to switch between pie chart analysis and performance comparison modes rather than displaying both simultaneously.

█ SETUP AND DISPLAY

For optimal visualization, users need to adjust the chart's display settings manually.

This involves:

Expanding the indicator window vertically to accommodate both the watchlist and graphical elements

Adjusting the Y-axis scale by dragging it to ensure proper spacing for the comparison panel grid

Modifying the X-axis scale to achieve the desired time window display

Fine-tuning these adjustments whenever switching between pie chart and comparison panel modes

These manual adjustments are necessary due to PineScript's limitations in controlling chart scaling programmatically. While this requires some initial setup, it allows users to customize the display to their preferred viewing proportions.

█ MAIN FEATURES

Distribution Analysis

The script provides three distinct distribution visualization modes through a pie chart.

Users can analyze their symbols by exchanges, asset types (such as Crypto, Forex, Futures), or market sectors.

If you can't see it well at first, adjust your chart scaling until it's displayed nicely.

Asset Exchanges

www.tradingview.com

Asset Types

Asset Sectors

The pie charts feature an optional 3D effect with adjustable depth and angle parameters. To enhance visual customization, four different color schemes are available: Default, Pastel, Dark, and Neon.

Each segment of the pie chart includes interactive tooltips that can be configured to show different levels of detail. Importantly, the pie chart only visualizes the distribution of selected assets (those marked with a checkmark in the watchlist), providing a focused view of the user's current interests.

Interactive Watchlist

The watchlist component displays real-time data for up to 10 user-defined symbols. Each entry shows current price, price changes (both absolute and percentage), volume metrics, and a comparison toggle.

The table is dynamically updated and features color-coded entries that correspond to their respective performance lines in the comparison chart. The watchlist serves as both an information display and a control panel for the comparison feature.

Performance Comparison

One of the script's most innovative features is its performance comparison panel.

Using polylines for smooth visualization, it tracks the 30-day performance of selected symbols relative to a 0% baseline.

The comparison chart includes a sophisticated grid system with 5% intervals and a dynamic legend showing current performance values.

The polyline implementation allows for fluid, continuous lines that accurately represent price movements, providing a more refined visual experience than traditional line plots. Like the pie charts, the comparison panel only displays performance lines for symbols that have been selected in the watchlist, allowing users to focus on their specific assets of interest.

█ TECHNICAL IMPLEMENTATION

The script utilizes several advanced PineScript features:

Dynamic array management for symbol tracking

Polyline-based charting for smooth performance visualization

Real-time data processing with security calls

Interactive tooltips and labels

Optimized drawing routines to maintain performance

Selective visualization based on user choices

█ CUSTOMIZATION

Users can personalize almost every aspect of the script:

Symbol selection and comparison preferences

Visual theme selection with four distinct color schemes

Pie chart dimensions and positioning

Tooltip information density

Component visibility toggles

█ LIMITATIONS

The primary limitation stems from PineScript's 500-line restriction per script.

This constraint necessitated the implementation of a mode-switching system between pie charts and the comparison panel, as displaying both simultaneously would exceed the line limit. Additionally, the script relies on manual chart scale adjustments, as PineScript doesn't provide direct control over chart scaling when overlay=false is enabled.

However, these limitations led to a more focused and efficient design approach that gives users control over their viewing experience.

█ CONCLUSION

All those tools exist in the native TradingView watchlist interface and they're better than what I just did.

However, now it exists in Pinescript... so I believe it's a win lol :)

Supertrend Alert with Arrows and Time FilterOverview

This script is designed to generate trading signals based on the Supertrend indicator, a popular technical analysis tool. The Supertrend indicator is used to identify the direction of the market trend and potential reversal points.

Supertrend Settings

The script uses two sets of Supertrend settings:

Small Supertrend

Factor: 3.0

ATR Period: 10

Big Supertrend

Factor: 10.0

ATR Period: 30

These settings are fixed and should not be altered to maintain the integrity of the signal generation process.

Configurable Parameters

startHour: The hour at which signal generation begins.

endHour: The hour at which signal generation ends.

These parameters allow users to focus on specific trading hours, optimizing the signal relevance to their trading strategy.

Signal Types

The script generates two types of signals:

Type 1: Reversal Signal

Long Signal: Triggered when the big Supertrend is in an uptrend, and the small Supertrend transitions from a downtrend to an uptrend.

Short Signal: Triggered when the big Supertrend is in a downtrend, and the small Supertrend transitions from an uptrend to a downtrend.

Type 2: Trend Change Signal

Long Signal: Triggered when the big Supertrend changes from a downtrend to an uptrend.

Short Signal: Triggered when the big Supertrend changes from an uptrend to a downtrend.

How the Script Works

Initialization: The script initializes with predefined Supertrend settings.

Data Input: Market data (e.g., price data) is fed into the script.

Supertrend Calculation: The script calculates the Supertrend values using the predefined factors and ATR periods.

Signal Detection: The script monitors the Supertrend values and detects the defined signals based on the conditions mentioned above.

Time Filtering: Signals are filtered based on the specified startHour and endHour, ensuring only relevant signals are displayed within the desired timeframe.

Usage

Set Parameters: Define startHour and endHour according to your trading schedule.

Run Script: Execute the script with market data input.

Interpret Signals: Monitor the generated signals and use them to inform your trading decisions.

Originality

Dual Supertrend Usage: The use of both a small and a big Supertrend to generate signals adds a layer of complexity and reliability to the signals.

Time-Based Filtering: Allows traders to focus on specific trading hours, enhancing the relevance and accuracy of signals.

Two Signal Types: The combination of reversal signals and trend change signals provides comprehensive market insights.

Conclusion

This Supertrend Signal Generator is a robust tool for traders seeking to leverage the Supertrend indicator for more informed trading decisions. By combining dual Supertrend settings and configurable trading hours, the script offers unique and flexible signal generation capabilities.

dashboard MTF,EMA User Guide: Dashboard MTF EMA

Script Installation:

Copy the script code.

Go to the script window (Pine Editor) on TradingView.

Paste the code into the script window.

Save the script.

Adding the Script to the Chart:

Return to your chart on TradingView.

Look for the script in the list of available scripts.

Add the script to the chart.

Interpreting the Table:

On the right side of the chart, you will see a table labeled "EMA" with arrows.

The rows correspond to different timeframes: 5 minutes (5M), 15 minutes (15M), 1 hour (1H), 4 hours (4H), and 1 day (1D).

Understanding the Arrows:

Each row of the table has two columns: "EMA" and an arrow.

"EMA" indicates the trend of the Exponential Moving Average (EMA) for the specified period.

The arrow indicates the direction of the trend: ▲ for bullish, ▼ for bearish.

Table Colors:

The colors of the table reflect the current trend based on the comparison between fast and slow EMAs.

Blue (▲) indicates a bullish trend.

Red (▼) indicates a bearish trend.

Table Theme:

The table has a dark (Dark) or light (Light) theme according to your preference.

The background, frame, and colors are adjusted based on the selected theme.

Usage:

Use the table as a quick indicator of trends on different timeframes.

The arrows help you quickly identify trends without navigating between different time units.

Designed to simplify analysis and avoid cluttering the chart with multiple indicators.

Pro Trading Art - Head And ShouldersHow the Script Works:

1. The script identifies potential Head and Shoulders patterns by searching for specific pivot highs and pivot lows in the price data.

2. It checks for the presence of a left shoulder, head, and right shoulder based on the conditions defined in the script.

3. If a valid Head and Shoulders pattern is found, the script plots lines and labels on the chart to visualize the pattern.

4. The script also identifies Inverted Head and Shoulders patterns using similar logic but with different conditions.

5. It plots lines and labels for the Inverted Head and Shoulders pattern.

6. The script generates short and long conditions based on the patterns. Short conditions trigger when the close price crosses below the neck level of a Head and Shoulders pattern, while long conditions trigger when the close price crosses above the neck level of an Inverted Head and Shoulders pattern.

7. It plots sell and buy signal shapes on the chart when the short and long conditions are met, respectively.

8. The script can also trigger alerts to notify the user when a valid Head and Shoulders or Inverted Head and Shoulders pattern is detected.

9. The script provides visual cues on the chart to help users identify potential trading opportunities.

10. The logic and parameters of the script can be modified by the user to customize the behavior and adapt it to different trading strategies.

How Users Can Make Profit Using This Script:

1. Identify potential short-selling opportunities: When a valid Head and Shoulders pattern is detected and a short condition is met, it indicates a potential trend reversal. Traders can consider opening short positions to profit from a downward price movement.

2. Identify potential long-buying opportunities: When a valid Inverted Head and Shoulders pattern is detected and a long condition is met, it suggests a potential trend reversal. Traders can consider opening long positions to profit from an upward price movement.

3. Combine with additional analysis: Users can utilize this script as a tool in their overall trading strategy. They can combine the signals generated by the script with other technical indicators, fundamental analysis, or market sentiment to make more informed trading decisions.

4. Define appropriate entry and exit points: Traders can use the lines and labels plotted by the script to determine entry and exit points for their trades. For example, they may choose to enter a short position after the price crosses below the neck level and exit when the price reaches a predetermined target or when the pattern is invalidated.

5. Set risk management measures: It is important for users to implement proper risk management strategies when trading based on the script's signals. They should define stop-loss orders to limit potential losses if the trade goes against them and consider setting profit targets to secure profits when the trade moves in their favor.

Strategy BackTest Display Statistics - TraderHalaiThis script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

Found an excellent display backtest engine by 'The Art of Trading'. This script is a snippet of his hard work, with some very minor tweaks and changes. Much respect to the original author.

Full credit to the original author of this script. It can be found here: www.tradingview.com

I decided to modify the script by simplifying it down and make it easier to integrate into existing strategies, using simple copy and paste, by relying on existing tradingview strategy backtester inputs. I have also added 3 additional performance metrics:

- Max Run Up

- Average Win per trade

- Average Loss per trade

As this is a work in progress, I will look to add in more performance metrics in future, as I further develop this script.

Feel free to use this display panel in your scripts and strategies.

Thanks and enjoy :)

Tick travel ⍗This script is a further exploration of 'ticks' (only on realtime - live bars), based on my previous script:

- www.tradingview.com -

What are 'ticks'?

... Once the script’s execution reaches the rightmost bar in the dataset, if trading is currently active on the chart’s symbol,

then Pine indicators will execute once every time an update occurs, i.e., price or volume changes ...

(www.tradingview.com)

This script has 2 parts:

1) Option: ' Tick up/down'

This is a further progression of previous work.

During bar development, every time there is an update (tick), a dot is placed.

If for example there is 1 tick (first of new bar), a dot will be placed on 1,

if it is the 8th tick off that bar, there will be a dot placed on 8.

While my previous script had the issue that there was an upper limit per bar (max 32),

this script (because it is working with labels) can place max 500 dots.

For each bar this is better, it has to be mentioned though that looking in history, once the limit of 500 has been reached,

you'll notice the last ones are being deleted. This is one of the reasons the script is not suitable for higher timeframes

(1h and higher, even higher than 5 minutes can give some issues if it is a highly traded ticker), if a bar would have more

than 500 ticks, they won't be drawn anymore (which is not desirable of course)

2) Option: ' Tick progression'

These are the same ticks, but placed on the candle itself, or you can show the candle:

Or 'without' candle (or 'black' colour):

When 'No candles' are enabled, the 'candles' get the colour at the right.

At the moment it is not possible to drawn between 2 candles, this technique uses labels with 'text',

each tick on a candle will have a 'space' added, so you can see a progression to the right.

Colours

- if price is higher than previous tick price -> green

- if price is lower than previous tick price -> red

- otherwise -> blue (dimmed)

There are options to choose the 'dot', when choosing 'custom',

just enter (copy/paste) your symbol of your choice in the 'custom' field:

Caveats:

- Labels and text will not always be exactly on the price itself

- The scripts needs more testings, possibly some ticks don't always get drawn as they should.

The lower the timeframe, the more possible issues can occur

- Since (candle option) the dots move to the right, the higher the timeframe and/or the more ticks,

the sooner ticks will go in the area of next candle.

That's why I made a separate 'start symbol'

-> This is the very first tick on each candle, then you can zoom in/out more easily until the dots don't merge into each other candle area:

A timeframe higher than 5 minutes mostly won't be feasible I believe

This script wouldn't be possible without the help of @LucF, also because of his script

With very much respect I am hugely inspired by him! Many Thanks to him, Tradingview, and everything associated with them!

Cheers!

logLibrary "log"

Logging library for easily displaying debug, info, warn, error and critical messages.

No real need to explain why you might want to use this library! I'm sure you've all experienced the frustration of trying to understand the data state of your scripts... so, enjoy! More on it's way...

(Don't forget to check the helpers in the script and the useful tips below)

Some Useful Tips

By default the log console persists between bars (for history) and bars and ticks (for realtime).

Sometimes it is useful to clear the log after each candle or tick (assuming we are using the above helpers):

```

log_print(clear = true) // starts afresh on every bar and tick (excludes historical bars but good realtime tick analysis)

log_print(clear = barstate.isnew) // clears the log at the start of each bar (again, excludes historical but good realtime candle analysis)

```

It is also useful to be able to selectively understand the state of data at specific points or times within a script:

```

if log.once()

debug('useful variable', my_var) // this log only gets written once, upon first execution of this statement

if log.only(5)

debug3(a, b, c) // these variables are only logged the first five times this statement is executed

log_print(clear = false) // clear must be false and you should not write other logs on every bar, or the above will be lost

```

Final tip. If you want to view ONLY log entries of a particular level, then negate the constant:

```

log_print(level = -LOG_DEBUG)

```

Detailed Interface

once() Restrict execution to only happen once. Usage: if assert.once()\n happens_once()

Returns: bool, true on first execution within scope, false subsequently

only(repeat) Restrict execution to happen a set number of times. Usage: if assert.only(5)\n happens_five_times()

Parameters:

repeat : int, the number of times to return true

Returns: bool, true for the set number of times within scope, false subsequently

init() Initialises the log array

Returns: string , tuple based array to contain all pending log entries (__LOG)

clear(msgs) Clears the log array

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

trace(msgs, msg) Writes a trace message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the trace message to write to the log

debug(msgs, msg) Writes a debug message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the debug message to write to the log

info(msgs, msg) Writes an info message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the info message to write to the log

warn(msgs, msg) Writes a warning message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the warn message to write to the log

error(msgs, msg) Writes an error message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the error message to write to the log

fatal(msgs, msg) Writes a critical message to the log console

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

msg : string, the fatal message to write to the log

log(msgs, level, msg) Write a log message to the log console with a custom level

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

level : ing, the logging level to assign to the message

msg : string, the log message to write to the log

severity(msgs) Checks the unprocessed log messages and returns the highest present level

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

Returns: int, the highest level found within the unfiltered logs

print(msgs, level, clear, rows, text_size, position) Prints all log messages to the screen

Parameters:

msgs : string , the current collection of unfiltered and unprocessed logs (__LOG)

level : int, the minimum required log level of each message to be displayed

clear : bool, clear the printed log console after each render (useful with realtime when set to barstate.isconfirmed)

rows : int, the number of rows to display in the log console

text_size : string, the text size of the log console (global size vars)

position : string, the position of the log console (global position vars)

unittest_log(case) Log module unit tests, for inclusion in parent script test suite. Usage: log.unittest_log(__ASSERTS)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

unittest(verbose) Run the log module unit tests as a stand alone. Usage: log.unittest()

Parameters:

verbose : bool, optionally disable the full report to only display failures

assertLibrary "assert"

Production ready assertions and auto-reporting for unit testing pine scripts.

This library was born from the need to maintain production level stability and catch regressions / bugs early and fast. I hope this help you trust your pine scripts too. More libraries and tools on their way... please follow for more.

Please see the script for helpers to copy into your own scripts as well as examples at the bottom of the library unit testing itself.

Quick Reference

```

case = assert.init()

new_case(case, 'Asserts for floats and ints')

assert.equal(a, b, case, 'a == b')

assert.not_equal(a, b, case, 'a != b')

assert.nan(a, case, 'a == na')

assert.not_nan(a, case, 'a != na')

assert.is_in(a, b, case, 'a in b ')

assert.is_not_in(a, b, case, 'a not in b ')

assert.array_equal(a, b, case, 'a == b ')

new_case(case, 'Asserts for ints only')

assert.int_in(a, b, case, 'a in b ')

assert.int_not_in(a, b, case, 'a not in b ')

assert.int_array_equal(a, b, case, 'a == b ')

new_case(case, 'Asserts for bools only')

assert.is_true(a, case, 'a == true')

assert.is_false(a, case, 'a == false')

assert.bool_equal(a, b, case, 'a == b')

assert.bool_not_equal(a, b, case, 'a != b')

assert.bool_nan(a, case, 'a == na')

assert.bool_not_nan(a, case, 'a != na')

assert.bool_array_equal(a, b, case, 'a == b ')

new_case(case, 'Asserts for strings only')

assert.str_equal(a, b, case, 'a == b')

assert.str_not_equal(a, b, case, 'a != b')

assert.str_nan(a, case, 'a == na')

assert.str_not_nan(a, case, 'a != na')

assert.str_in(a, b, case, 'a in b ')

assert.str_not_in(a, b, case, 'a not in b ')

assert.str_array_equal(a, b, case, 'a == b ')

assert.report(case)

```

Detailed Interface

once() Restrict execution to only happen once. Usage: if assert.once()\n happens_once()

Returns: bool, true on first execution within scope, false subsequently

init() Initialises the asserts array

Returns: string , tuple based array containing all unit test results and current case details (__ASSERTS)

equal(a, b, case, name) Numeric assert equal. Usage: assert.equal(1, 1, case, 'one == one')

Parameters:

a : float, numeric value "a" to compare equal to "b"

b : float, numeric value "b" to compare equal to "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

not_equal(a, b, case, name) Numeric assert not equal. Usage: assert.not_equal(1, 2, case, 'one != two')

Parameters:

a : float, numeric value "a" to compare not equal "b"

b : float, numeric value "b" to compare not equal "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

nan(a, case, name) Numeric assert is NaN. Usage: assert.nan(float(na), case, 'number is NaN')

Parameters:

a : float, numeric value "a" to check is NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

not_nan(a, case, name) Numeric assert is not NaN. Usage: assert.not_nan(1, case, 'number is not NaN')

Parameters:

a : float, numeric value "a" to check is not NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

is_in(a, b, case, name) Numeric assert value in float array. Usage: assert.is_in(1, array.from(1.0), case, '1 is in ')

Parameters:

a : float, numeric value "a" to check is in array "b"

b : float , array "b" to check contains "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

is_not_in(a, b, case, name) Numeric assert value not in float array. Usage: assert.is_not_in(2, array.from(1.0), case, '2 is not in ')

Parameters:

a : float, numeric value "a" to check is not in array "b"

b : float , array "b" to check does not contain "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

array_equal(a, b, case, name) Float assert arrays are equal. Usage: assert.array_equal(array.from(1.0), array.from(1.0), case, ' == ')

Parameters:

a : float , array "a" to check is identical to array "b"

b : float , array "b" to check is identical to array "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

int_in(a, b, case, name) Integer assert value in integer array. Usage: assert.int_in(1, array.from(1), case, '1 is in ')

Parameters:

a : int, value "a" to check is in array "b"

b : int , array "b" to check contains "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

int_not_in(a, b, case, name) Integer assert value not in integer array. Usage: assert.int_not_in(2, array.from(1), case, '2 is not in ')

Parameters:

a : int, value "a" to check is not in array "b"

b : int , array "b" to check does not contain "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

int_array_equal(a, b, case, name) Integer assert arrays are equal. Usage: assert.int_array_equal(array.from(1), array.from(1), case, ' == ')

Parameters:

a : int , array "a" to check is identical to array "b"

b : int , array "b" to check is identical to array "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

is_true(a, case, name) Boolean assert is true. Usage: assert.is_true(true, case, 'is true')

Parameters:

a : bool, value "a" to check is true

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

is_false(a, case, name) Boolean assert is false. Usage: assert.is_false(false, case, 'is false')

Parameters:

a : bool, value "a" to check is false

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

bool_equal(a, b, case, name) Boolean assert equal. Usage: assert.bool_equal(true, true, case, 'true == true')

Parameters:

a : bool, value "a" to compare equal to "b"

b : bool, value "b" to compare equal to "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

bool_not_equal(a, b, case, name) Boolean assert not equal. Usage: assert.bool_not_equal(true, false, case, 'true != false')

Parameters:

a : bool, value "a" to compare not equal "b"

b : bool, value "b" to compare not equal "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

bool_nan(a, case, name) Boolean assert is NaN. Usage: assert.bool_nan(bool(na), case, 'bool is NaN')

Parameters:

a : bool, value "a" to check is NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

bool_not_nan(a, case, name) Boolean assert is not NaN. Usage: assert.bool_not_nan(true, case, 'bool is not NaN')

Parameters:

a : bool, value "a" to check is not NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

bool_array_equal(a, b, case, name) Boolean assert arrays are equal. Usage: assert.bool_array_equal(array.from(true), array.from(true), case, ' == ')

Parameters:

a : bool , array "a" to check is identical to array "b"

b : bool , array "b" to check is identical to array "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_equal(a, b, case, name) String assert equal. Usage: assert.str_equal('hi', 'hi', case, '"hi" == "hi"')

Parameters:

a : string, value "a" to compare equal to "b"

b : string, value "b" to compare equal to "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_not_equal(a, b, case, name) String assert not equal. Usage: assert.str_not_equal('hi', 'bye', case, '"hi" != "bye"')

Parameters:

a : string, value "a" to compare not equal "b"

b : string, value "b" to compare not equal "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_nan(a, case, name) String assert is NaN. Usage: assert.str_nan(string(na), case, 'string is NaN')

Parameters:

a : string, value "a" to check is NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_not_nan(a, case, name) String assert is not NaN. Usage: assert.str_not_nan('hi', case', 'string is not NaN')

Parameters:

a : string, value "a" to check is not NaN

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_in(a, b, case, name) String assert value in string array. Usage: assert.str_in('hi', array.from('hi'), case, '"hi" in ')

Parameters:

a : string, value "a" to check is in array "b"

b : string , array "b" to check contains "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_not_in(a, b, case, name) String assert value not in string array. Usage: assert.str_in('hi', array.from('bye'), case, '"hi" in ')

Parameters:

a : string, value "a" to check is not in array "b"

b : string , array "b" to check does not contain "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

str_array_equal(a, b, case, name) String assert arrays are equal. Usage: assert.str_array_equal(array.from('hi'), array.from('hi'), case, ' == ')

Parameters:

a : string , array "a" to check is identical to array "b"

b : string , array "b" to check is identical to array "a"

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the current unit test name, if undefined the test index of the current case is used

Returns: bool, true if the assertion passes, false otherwise

new_case(case, name) Assign a new test case name, for the next set of unit tests. Usage: assert.new_case(case, 'My tests')

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

name : string, the case name for the next suite of tests

clear(case) Clear all stored unit tests from all cases. Usage: assert.clear(case)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

revert(case) Revert the previous unit test. Usage: = assert.revert(case)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

Returns: , tuple containing the msg and result of the reverted test

passed(case, revert) Check if the last unit test has passed. Usage: bool success = assert.passed(case)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

revert : bool, optionally revert the test

Returns: bool, true only if the test passed

failed(case, revert) Check if the last unit test has failed. Usage: bool failure = assert.failed(case)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

revert : bool, optionally revert the test

Returns: bool, true only if the test failed

report(case, verbose) Report the outcome of unit tests that fail. Usage: bool passed = assert.report(case)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

verbose : bool, optionally display full report that includes the outcome of all tests

Returns: bool, true only if all tests passed

unittest_assert(case) Assert module unit tests, for inclusion in parent script test suite. Usage: assert.unittest_assert(__ASSERTS)

Parameters:

case : string , the current test case and array of previous unit tests (__ASSERTS)

unittest(verbose) Run the assert module unit tests as a stand alone. Usage: assert.unittest()

Parameters:

verbose : bool, optionally toggle report to display the outcome of all unit tests

Matrix Library (Linear Algebra, incl Multiple Linear Regression)What's this all about?

Ever since 1D arrays were added to Pine Script, many wonderful new opportunities have opened up. There has been a few implementations of matrices and matrix math (most notably by TradingView-user tbiktag in his recent Moving Regression script: ). However, so far, no comprehensive libraries for matrix math and linear algebra has been developed. This script aims to change that.

I'm not math expert, but I like learning new things, so I took it upon myself to relearn linear algebra these past few months, and create a matrix math library for Pine Script. The goal with the library was to make a comprehensive collection of functions that can be used to perform as many of the standard operations on matrices as possible, and to implement functions to solve systems of linear equations. The library implements matrices using arrays, and many standard functions to manipulate these matrices have been added as well.

The main purpose of the library is to give users the ability to solve systems of linear equations (useful for Multiple Linear Regression with K number of independent variables for example), but it can also be used to simulate 2D arrays for any purpose.

So how do I use this thing?

Personally, what I do with my private Pine Script libraries is I keep them stored as text-files in a Libraries folder, and I copy and paste them into my code when I need them. This library is quite large, so I have made sure to use brackets in comments to easily hide any part of the code. This helps with big libraries like this one.

The parts of this script that you need to copy are labeled "MathLib", "ArrayLib", and "MatrixLib". The matrix library is dependent on the functions from these other two libraries, but they are stripped down to only include the functions used by the MatrixLib library.

When you have the code in your script (pasted somewhere below the "study()" call), you can create a matrix by calling one of the constructor functions. All functions in this library start with "matrix_", and all constructors start with either "create" or "copy". I suggest you read through the code though. The functions have very descriptive names, and a short description of what each function does is included in a header comment directly above it. The functions generally come in the following order:

Constructors: These are used to create matrices (empy with no rows or columns, set shape filled with 0s, from a time series or an array, and so on).

Getters and setters: These are used to get data from a matrix (like the value of an element or a full row or column).

Matrix manipulations: These functions manipulate the matrix in some way (for example, functions to append columns or rows to a matrix).

Matrix operations: These are the matrix operations. They include things like basic math operations for two indices, to transposing a matrix.

Decompositions and solvers: Next up are functions to solve systems of linear equations. These include LU and QR decomposition and solvers, and functions for calculating the pseudo-inverse or inverse of a matrix.

Multiple Linear Regression: Lastly, we find an implementation of a multiple linear regression, including all the standard statistics one can expect to find in most statistical software packages.

Are there any working examples of how to use the library?

Yes, at the very end of the script, there is an example that plots the predictions from a multiple linear regression with two independent (explanatory) X variables, regressing the chart data (the Y variable) on these X variables. You can look at this code to see a real-world example of how to use the code in this library.

Are there any limitations?

There are no hard limiations, but the matrices uses arrays, so the number of elements can never exceed the number of elements supported by Pine Script (minus 2, since two elements are used internally by the library to store row and column count). Some of the operations do use a lot of resources though, and as a result, some things can not be done without timing out. This can vary from time to time as well, as this is primarily dependent on the available resources from the Pine Script servers. For instance, the multiple linear regression cannot be used with a lookback window above 10 or 12 most of the time, if the statistics are reported. If no statistics are reported (and therefore not calculated), the lookback window can usually be extended to around 60-80 bars before the servers time out the execution.

Hopefully the dev-team at TradingView sees this script and find ways to implement this functionality diretly into Pine Script, as that would speed up many of the operations and make things like MLR (multiple linear regression) possible on a bigger lookback window.

Some parting words

This library has taken a few months to write, and I have taken all the steps I can think of to test it for bugs. Some may have slipped through anyway, so please let me know if you find any, and I'll try my best to fix them when I have time to do so. This library is intended to help the community. Therefore, I am releasing the library as open source, in the hopes that people may improving on it, or using it in their own work. If you do make something cool with this, or if you find ways to improve the code, please let me know in the comments.

EMA TrendThe purpose of this script is to identify price trends based on EMAs. The relative position of price to specific EMAs and the position of certain EMAs towards each other are used to determine the trend direction. The script is intended for investors as a tool to define a basis for further evaluation. I do not use the script as a signal generator and would not recommend doing so without the help of additional indicators.

How to work with the script

The major (or long term) trend direction is determined by the 144 EMA much in the same way as the 200 MA is used in other systems. If the price is above the 144 EMA we are in a long term uptrend, below we are in a long term downtrend. This is to be taken with a grain of salt though. The 144 EMA is considerably shorter than the 200 SMA and is more prone to the price fluctuating around it during periods without a strong long term trend. I recommend using this as a confirmation for the short term trend.

The short term trend is derived from the position and slope of the price, the 21 EMA and the 55 EMA. If the price is above the 21 EMA, the 21 above the 55 EMA, both EMAs are sloping upwards and the distance between the two is increasing, we are talking about an uptrend (and vice versa for a downtrend). This is visualized by the color of the fill between the 144 EMA and close price. Green for uptrend, red for downtrend and no color for an undetermined trend.

The EMAs used are: 21 , 34 , 55 , 89 , 144 , 233 . Most of the EMAs are at 50 transparency to appear less dominant. For orientation, the 144 EMA is bright green to indicate its general importance for the trend determination, and the 55 EMAs is not transparent mainly to be able to identify positioning when the EMAs are close together.

Base time frame EMA

The 144 EMA is plotted twice where one is fixed to the daily time frame (can be configured) to be able to have the 144 on different timeframes during analysis. I find this very useful to keep the focus on my main time frame while analyzing trend on lower or higher time frames. This can also be turned off.

Configurability

This script is less configurable than I generally like with my other scripts. The reason is that the title attribute of the plots is not dynamic, and I use the data window often to get exact values from the script to determine buy targets for pullbacks and other things. Hence, I prefer not to have random names (or no names) in there to save mental capacity. If this ever becomes available, I'll gladly add this to this script. Till then, I encourage you to take the script and adjust it to your own needs. It should be simple enough even if you are just starting out in pine.

Waindrops [Makit0]█ OVERALL

Plot waindrops (custom volume profiles) on user defined periods, for each period you get high and low, it slices each period in half to get independent vwap, volume profile and the volume traded per price at each half.

It works on intraday charts only, up to 720m (12H). It can plot balanced or unbalanced waindrops, and volume profiles up to 24H sessions.

As example you can setup unbalanced periods to get independent volume profiles for the overnight and cash sessions on the futures market, or 24H periods to get the full session volume profile of EURUSD

The purpose of this indicator is twofold:

1 — from a Chartist point of view, to have an indicator which displays the volume in a more readable way

2 — from a Pine Coder point of view, to have an example of use for two very powerful tools on Pine Script:

• the recently updated drawing limit to 500 (from 50)

• the recently ability to use drawings arrays (lines and labels)

If you are new to Pine Script and you are learning how to code, I hope you read all the code and comments on this indicator, all is designed for you,

the variables and functions names, the sometimes too big explanations, the overall structure of the code, all is intended as an example on how to code

in Pine Script a specific indicator from a very good specification in form of white paper

If you wanna learn Pine Script form scratch just start HERE

In case you have any kind of problem with Pine Script please use some of the awesome resources at our disposal: USRMAN , REFMAN , AWESOMENESS , MAGIC

█ FEATURES

Waindrops are a different way of seeing the volume and price plotted in a chart, its a volume profile indicator where you can see the volume of each price level

plotted as a vertical histogram for each half of a custom period. By default the period is 60 so it plots an independent volume profile each 30m

You can think of each waindrop as an user defined candlestick or bar with four key values:

• high of the period

• low of the period

• left vwap (volume weighted average price of the first half period)

• right vwap (volume weighted average price of the second half period)

The waindrop can have 3 different colors (configurable by the user):

• GREEN: when the right vwap is higher than the left vwap (bullish sentiment )

• RED: when the right vwap is lower than the left vwap (bearish sentiment )

• BLUE: when the right vwap is equal than the left vwap ( neutral sentiment )

KEY FEATURES

• Help menu

• Custom periods

• Central bars

• Left/Right VWAPs

• Custom central bars and vwaps: color and pixels

• Highly configurable volume histogram: execution window, ticks, pixels, color, update frequency and fine tuning the neutral meaning

• Volume labels with custom size and color

• Tracking price dot to be able to see the current price when you hide your default candlesticks or bars

█ SETTINGS

Click here or set any impar period to see the HELP INFO : show the HELP INFO, if it is activated the indicator will not plot

PERIOD SIZE (max 2880 min) : waindrop size in minutes, default 60, max 2880 to allow the first half of a 48H period as a full session volume profile

BARS : show the central and vwap bars, default true

Central bars : show the central bars, default true

VWAP bars : show the left and right vwap bars, default true

Bars pixels : width of the bars in pixels, default 2

Bars color mode : bars color behavior

• BARS : gets the color from the 'Bars color' option on the settings panel

• HISTOGRAM : gets the color from the Bearish/Bullish/Neutral Histogram color options from the settings panel

Bars color : color for the central and vwap bars, default white

HISTOGRAM show the volume histogram, default true

Execution window (x24H) : last 24H periods where the volume funcionality will be plotted, default 5

Ticks per bar (max 50) : width in ticks of each histogram bar, default 2

Updates per period : number of times the histogram will update

• ONE : update at the last bar of the period

• TWO : update at the last bar of each half period

• FOUR : slice the period in 4 quarters and updates at the last bar of each of them

• EACH BAR : updates at the close of each bar

Pixels per bar : width in pixels of each histogram bar, default 4

Neutral Treshold (ticks) : delta in ticks between left and right vwaps to identify a waindrop as neutral, default 0

Bearish Histogram color : histogram color when right vwap is lower than left vwap, default red

Bullish Histogram color : histogram color when right vwap is higher than left vwap, default green

Neutral Histogram color : histogram color when the delta between right and left vwaps is equal or lower than the Neutral treshold, default blue

VOLUME LABELS : show volume labels

Volume labels color : color for the volume labels, default white

Volume Labels size : text size for the volume labels, choose between AUTO, TINY, SMALL, NORMAL or LARGE, default TINY

TRACK PRICE : show a yellow ball tracking the last price, default true

█ LIMITS

This indicator only works on intraday charts (minutes only) up to 12H (720m), the lower chart timeframe you can use is 1m

This indicator needs price, time and volume to work, it will not work on an index (there is no volume), the execution will not be allowed

The histogram (volume profile) can be plotted on 24H sessions as limit but you can plot several 24H sessions

█ ERRORS AND PERFORMANCE

Depending on the choosed settings, the script performance will be highly affected and it will experience errors

Two of the more common errors it can throw are:

• Calculation takes too long to execute

• Loop takes too long

The indicator performance is highly related to the underlying volatility (tick wise), the script takes each candlestick or bar and for each tick in it stores the price and volume, if the ticker in your chart has thousands and thousands of ticks per bar the indicator will throw an error for sure, it can not calculate in time such amount of ticks.

What all of that means? Simply put, this will throw error on the BITCOIN pair BTCUSD (high volatility with tick size 0.01) because it has too many ticks per bar, but lucky you it will work just fine on the futures contract BTC1! (tick size 5) because it has a lot less ticks per bar

There are some options you can fine tune to boost the script performance, the more demanding option in terms of resources consumption is Updates per period , by default is maxed out so lowering this setting will improve the performance in a high way.

If you wanna know more about how to improve the script performance, read the HELP INFO accessible from the settings panel

█ HOW-TO SETUP

The basic parameters to adjust are Period size , Ticks per bar and Pixels per bar

• Period size is the main setting, defines the waindrop size, to get a better looking histogram set bigger period and smaller chart timeframe

• Ticks per bar is the tricky one, adjust it differently for each underlying (ticker) volatility wise, for some you will need a low value, for others a high one.

To get a more accurate histogram set it as lower as you can (min value is 1)

• Pixels per bar allows you to adjust the width of each histogram bar, with it you can adjust the blank space between them or allow overlaping

You must play with these three parameters until you obtain the desired histogram: smoother, sharper, etc...

These are some of the different kind of charts you can setup thru the settings:

• Balanced Waindrops (default): charts with waindrops where the two halfs are of same size.

This is the default chart, just select a period (30m, 60m, 120m, 240m, pick your poison), adjust the histogram ticks and pixels and watch

• Unbalanced Waindrops: chart with waindrops where the two halfs are of different sizes.

Do you trade futures and want to plot a waindrop with the first half for the overnight session and the second half for the cash session? you got it;

just adjust the period to 1860 for any CME ticker (like ES1! for example) adjust the histogram ticks and pixels and watch

• Full Session Volume Profile: chart with waindrops where only the first half plots.

Do you use Volume profile to analize the market? Lucky you, now you can trick this one to plot it, just try a period of 780 on SPY, 2760 on ES1!, or 2880 on EURUSD

remember to adjust the histogram ticks and pixels for each underlying

• Only Bars: charts with only central and vwap bars plotted, simply deactivate the histogram and volume labels

• Only Histogram: charts with only the histogram plotted (volume profile charts), simply deactivate the bars and volume labels

• Only Volume: charts with only the raw volume numbers plotted, simply deactivate the bars and histogram

If you wanna know more about custom full session periods for different asset classes, read the HELP INFO accessible from the settings panel

EXAMPLES

Full Session Volume Profile on MES 5m chart:

Full Session Unbalanced Waindrop on MNQ 2m chart (left side Overnight session, right side Cash Session):

The following examples will have the exact same charts but on four different tickers representing a futures contract, a forex pair, an etf and a stock.

We are doing this to be able to see the different parameters we need for plotting the same kind of chart on different assets

The chart composition is as follows:

• Left side: Volume Labels chart (period 10)

• Upper Right side: Waindrops (period 60)

• Lower Right side: Full Session Volume Profile

The first example will specify the main parameters, the rest of the charts will have only the differences

MES :

• Left: Period size: 10, Bars: uncheck, Histogram: uncheck, Execution window: 1, Ticks per bar: 2, Updates per period: EACH BAR,

Pixels per bar: 4, Volume labels: check, Track price: check

• Upper Right: Period size: 60, Bars: check, Bars color mode: HISTOGRAM, Histogram: check, Execution window: 2, Ticks per bar: 2,

Updates per period: EACH BAR, Pixels per bar: 4, Volume labels: uncheck, Track price: check

• Lower Right: Period size: 2760, Bars: uncheck, Histogram: check, Execution window: 1, Ticks per bar: 1, Updates per period: EACH BAR,

Pixels per bar: 2, Volume labels: uncheck, Track price: check

EURUSD :

• Upper Right: Ticks per bar: 10

• Lower Right: Period size: 2880, Ticks per bar: 1, Pixels per bar: 1

SPY :

• Left: Ticks per bar: 3

• Upper Right: Ticks per bar: 5, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 2, Pixels per bar: 2

AAPL :

• Left: Ticks per bar: 2

• Upper Right: Ticks per bar: 6, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 1, Pixels per bar: 2

█ THANKS TO

PineCoders for all they do, all the tools and help they provide and their involvement in making a better community

scarf for the idea of coding a waindrops like indicator, I did not know something like that existed at all

All the Pine Coders, Pine Pros and Pine Wizards, people who share their work and knowledge for the sake of it and helping others, I'm very grateful indeed

I'm learning at each step of the way from you all, thanks for this awesome community;

Opensource and shared knowledge: this is the way! (said with canned voice from inside my helmet :D)

█ NOTE

This description was formatted following THIS guidelines

═════════════════════════════════════════════════════════════════════════

I sincerely hope you enjoy reading and using this work as much as I enjoyed developing it :D

GOOD LUCK AND HAPPY TRADING!

Multi-Session Volume Profile [MarkitTick]💡 This comprehensive Multi-Session Volume Profile indicator offers a sophisticated, array-based approach to Auction Market Theory. By simultaneously processing Daily, Weekly, Monthly, and Custom Session profiles, it empowers traders to visualize the migration of value across multiple timeframes without the performance overhead of standard heavy profile scripts. It is designed to identify key liquidity nodes, support/resistance zones defined by volume, and the directional bias of the market through Point of Control (POC) shifts.

✨ Originality and Utility

● Multi-Dimensional Value Analysis